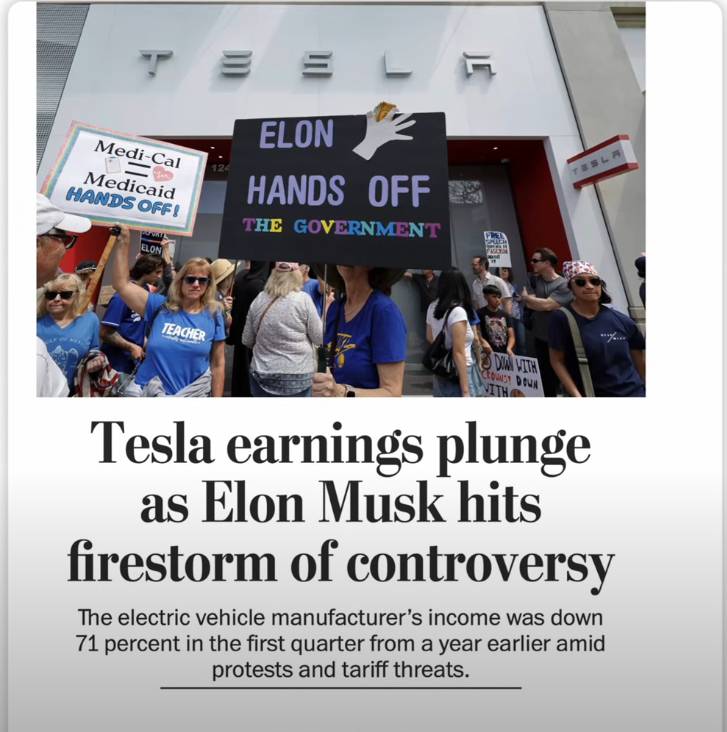

Tesla Incorporated reported a steep downturn in its financial results for the initial quarter of 2024. The electric vehicle manufacturer experienced a significant 71 percent plunge in net income compared to the same period last year. This sharp decline highlights mounting difficulties for the company, stemming from a combination of factors including reputational headwinds linked to its CEO, stiffer competition within the automotive sector, and an aging product lineup. The announced figures paint a picture of a company navigating increasingly turbulent waters as it attempts to maintain its market position and deliver on past promises.

Financial Performance Falls Short

The severity of Tesla's situation is underscored by its failure to meet market expectations. Beyond the dramatic 71 percent reduction in net income, the company's earnings per share came in at 27 cents, considerably lower than the 41 cents analysts had projected. Similarly, reported revenue of 19.34 billion dollars fell significantly short of the 21.11 billion dollars anticipated by Wall Street. These disappointing results are particularly concerning as they occurred even after many financial analysts had already tempered their forecasts, indicating the depth of the company's current struggles to sustain previous growth levels.

Musk's Influence and Market Pressures

Controversies surrounding Chief Executive Elon Musk appear to be impacting consumer perception and contributing to the difficulties. Tesla itself acknowledged that changing political sentiment could meaningfully affect demand for its vehicles soon. Furthermore, the company cited external economic pressures, noting that uncertainty in the automotive and energy markets continues to rise. Rapidly evolving international trade policies and global supply chain disruptions were mentioned as factors adversely affecting Tesla's cost structure and operational stability, adding layers of complexity to its business environment.

Aging Products and Competitive Landscape

Tesla also faces challenges from its own product portfolio and the broader market. The company currently lacks fresh models to excite consumers, relying on an aging vehicle portfolio while competitors consistently introduce new electric vehicles. Sales figures reflect this, with quarterly shipments dropping approximately 22 percent in China and deliveries sinking 62 percent in Germany. The firm's continued reliance on promoting future concepts like robotaxis and humanoid robots contrasts sharply with the tangible new offerings from rival carmakers, potentially weakening its immediate appeal to buyers seeking the latest innovations.

Underlying Profitability and Future Uncertainty

Beneath the headline figures, the financial picture requires scrutiny. Tesla continues to generate substantial income each quarter from selling regulatory credits, amounting to 595 million dollars in the latest period. Stripping out these credits, along with net interest income and other adjustments, reveals a pre-tax operational deficit of approximately 200 million dollars for the quarter. In response to these pressures, Tesla is signaling caution, pledging to revisit its 2025 growth outlook. Efforts to spur sales include releasing a less-expensive Cybertruck version and developing a lower-cost Model Y variant.